CVX Stock: Chevron’s 2025 Outlook, Risks, and Opportunities

Chevron Corporation (CVX) has been a major focus in the energy stock market throughout 2025. Investors tracking CVX stock have seen mixed signals as the company navigates a volatile macroeconomic landscape, shifting oil prices, and evolving industry dynamics. This article highlights the latest performance, key risks, and strategic opportunities surrounding CVX stock.

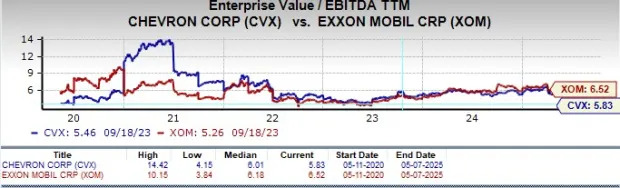

Recent Performance of CVX Stock

Chevron released its Q1 2025 earnings, revealing performance that beat expectations on earnings per share but missed revenue estimates. Adjusted earnings came in at $2.18 per share—slightly above forecasts but down 26% year-over-year. Revenue dropped by 2.3%, reaching $47.6 billion. These results have left investors uncertain, as CVX stock currently trades just above $135, hovering near its 52-week low of $132.04. Compared to competitors, CVX has underperformed, with shares down 15% over the past three years, while ExxonMobil gained 24% in the same period. For a comprehensive breakdown, visit After Q1 Results, What Comes Next for Chevron Shareholders?.

Key Risks and Challenges Facing Chevron

Several challenges are weighing on CVX stock. Concerns about peak Permian Basin production, declining cash flow, and rising company debt have sparked debates about the stock's fair valuation. In Q1, Chevron's free cash flow fell to $1.3 billion and the company reduced its share buyback target for Q2 from $3.9 billion to $2.5–$3 billion. This decision reflects a shaky macro environment and Brent crude’s slide toward $60 per barrel. For a deeper dive into these risks, including analyst opinions on why Chevron may be a sell, read Chevron Stock Valuation At Risk From Cash Flow Pressures (CVX) | Seeking Alpha.

Operational Highlights and Strategic Assets

Despite short-term headwinds, Chevron maintains a resilient asset portfolio. In its Q1 report, the company noted that U.S. net oil-equivalent production rose by 63,000 barrels per day year-over-year. The Permian Basin remains a core strength, with 80% of the acreage requiring low or no royalty payments—boosting long-term returns. International projects, such as the Tengiz field in Kazakhstan and deepwater Gulf of Mexico ventures, further strengthen Chevron’s production profile. Details are available at Chevron Reveals Q1 Net Oil Equivalent Production Level | Rigzone.

Financial Health and Capital Management

Chevron continues to exercise disciplined capital management. In Q1 2025, capital expenditures totaled just $3.9 billion. The company has also committed to $2–$3 billion in cost reductions by 2026. With a debt-to-capital ratio around 16.6%, Chevron’s balance sheet is among the strongest in the sector. Its ability to maintain dividend payouts and consistent buybacks demonstrates commitment to shareholder returns, though the sustainability of these returns will depend on future commodity price trends.

Conclusion: Is CVX Stock a Buy for 2025?

CVX stock stands at a crossroads in 2025. While risks linger—especially with softening oil prices and concerns about cash flow—Chevron’s leading assets, prudent cost management, and robust financial position offer a degree of stability. Investors should monitor upcoming quarters closely and leverage detailed analysis from trusted sources to make informed decisions regarding CVX stock. Stay updated with performance and strategic shifts by following industry news and expert commentary.